Every business owner needs some basic estate planning documents, even if you are not married, have no-one financially dependent upon you, or your business is not worth much yet. You should consider the potential value of your business, and recognise that it is dependent upon you If you have a spouse, life partner, or children, you definitely need to consider estate planning documents to provide for what would happen if you die or become incapacitated.

Here are the documents you may need to obtain:

Enduring Power of Attorney

This document gives another person power (your agent) to handle your finances in your absence. This may include paying your bills, negotiating a lease, dealing with employees, contractors & government departments, or working with your bank. You can give your agent power immediately or only upon your incapacity.

Medical Power of Attorney

Everyone age 18 and over should have this document. It names & empowers the person you want to make medical decisions for you, if you cannot do it for yourself. Do yourself & your loved ones a BIG favour, and create this now.

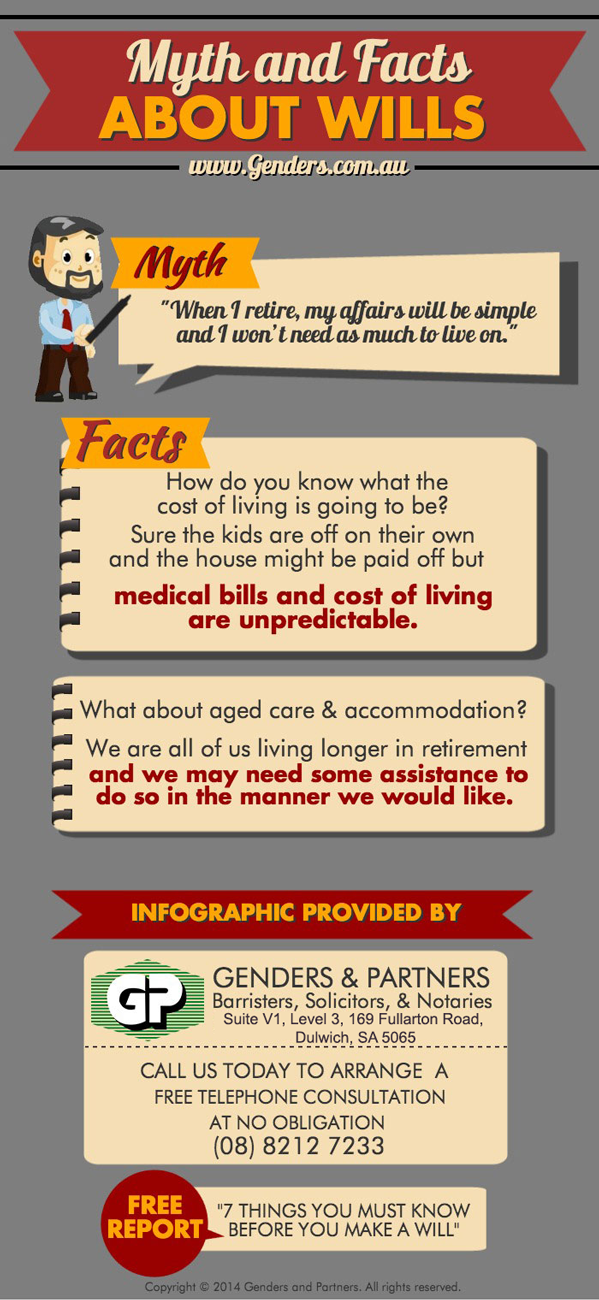

Will

Your Will says who you want to receive your assets after you die, who should handle your affairs upon your passing, and who you want to be a guardian for your children. This must be formally executed to be valid, typically with 2 witnesses, depending upon state law. Everyone should have a Will.

Other Documents

Some of you may need other documents, such as discretionary trusts, property agreements, co-habitation agreements, pre-nuptial agreements, irrevocable trusts, special needs trusts, superannuation trusts or life insurance trusts.